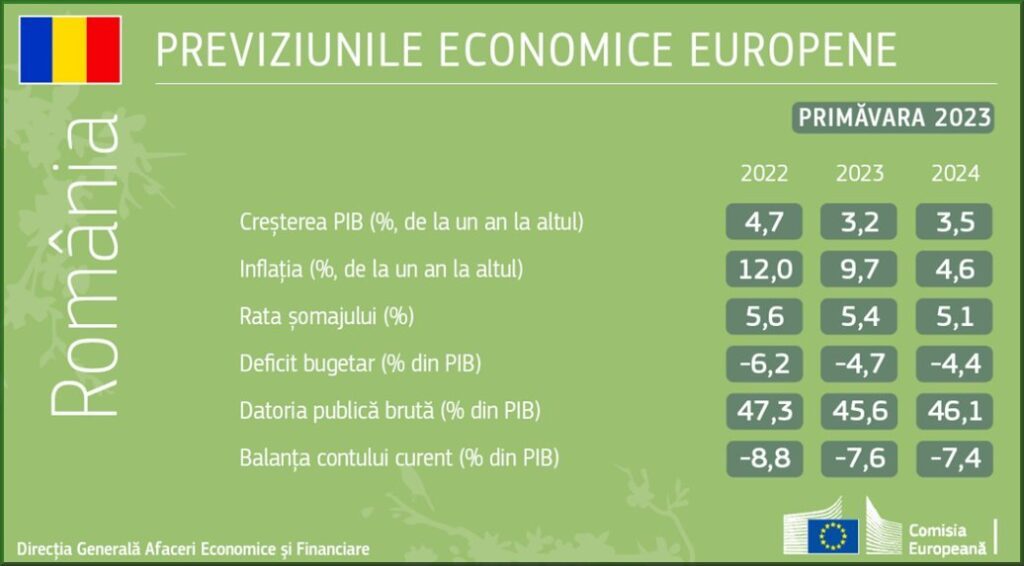

One raises the economic growth forecast from 2.5% to 3.2% in 2023. Inflation falls below 10% and budget deficit reaches 4.7% of GDP

The European Commission believes the Romanian economy will grow more strongly than previously expected and has raised its forecast for real GDP growth from 2.5% to 3.2% in 2023.

“Economic growth will continue, albeit at a slower pace than in 2022, due to persistent inflation, tight financing conditions and low growth in trading partners. Core inflation is expected to peak in 2023 and overall inflation will remain above the inflation target over the forecast period. Unemployment is estimated to decline only marginally, keeping the labor market relatively tight and wage growth high,” European Commission economists summarized the forecast.

What the European Commission says about Romania in the spring 2023 economic forecast:

Resilient growth despite headwinds

Growth reached 4.7% in 2022, driven by strong private consumption and robust investment. High-frequency indicators point to a reasonably resilient economy in 2023-Q1, with rising retail sales sentiment and sales and signs of improvement in industrial production. Employment expectations remained at a relatively high level.

Going forward, high inflation, tight financing conditions and lower growth in trading partners will all slow real growth. Despite these headwinds, private consumption growth is expected to remain positive thanks to higher wages and pensions and the extension of the energy price ceiling until 2025. Government support schemes and a resilient labor market will also support economic activity.

Monetary policy should remain tight, with monetary policy rates at 7%, affecting the flow of credit to the economy and investment. However, planned investments under the National Recovery and Resilience Plan (PNRR) and inflows from other EU funds can cushion the impact of tight credit conditions. Investment is expected to strongly support real growth in 2023 and 2024.

It is estimated that net exports will not contribute to GDP growth. Despite lower energy prices and improved terms of trade, strong domestic demand will keep the trade balance negative. The current account deficit is projected to remain around [8%] of GDP over the forecast period, posing medium-term external sustainability risks.

All in all, real GDP is estimated to grow 3.2% in 2023 and 3.5% in 2024. Risks to the forecast are downside, as delays in NRDP implementation may reduce investment.

“Sticky” unemployment and wage pressure

Despite solid GDP growth, employment prospects remain modest, as an aging population and mass migration pose serious obstacles to job creation. However, labor market integration of people fleeing the war in Ukraine and visas for non-EU workers may be mitigating factors. The unemployment rate is expected to fall slightly, to 5.4% in 2023 and 5.1% in 2024. Wage growth was strong, especially in the private sector, but for the economy as a whole, overall CPI inflation lags. The tight labor market, the need to compensate for purchasing power losses and high inflation should contribute to substantial wage increases in 2023 and 2024.

Core inflation remains high

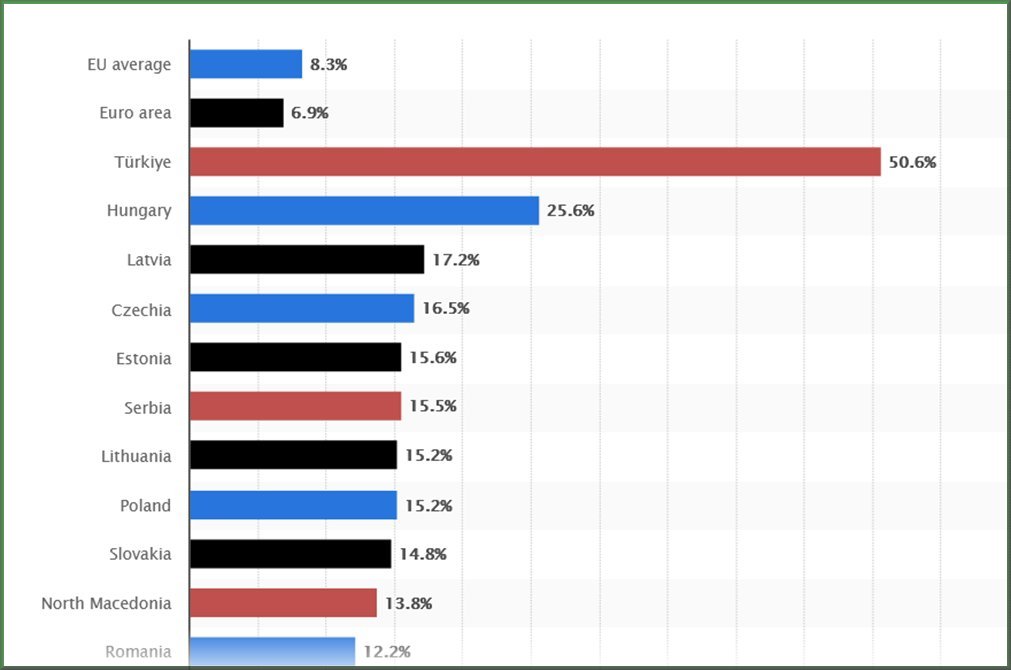

Overall HICP inflation (according to the EU Harmonized Index 0 n.ed.) peaked in November and then fell to 12.2% in March due to lower energy prices. Because of the energy price cap scheme, almost no change is expected for this component, largely driven by movements in fuel and energy distribution prices. However, core inflation continued to rise due to increases in processed food and services. After peaking in the first quarter, inflation is expected to remain above headline inflation this year. All in all, average HICP inflation will fall to 9.7% in 2023 and 4.6% in 2024, but the risks are to the upside as upward wage pressures are high.

Romanian government deficit expected to decrease

Romania’s public deficit is estimated to fall from 6.2% in 2022 to 4.7% of GDP in 2023 (in ESA terms, according to the European methodology – ed.). Robust nominal GDP growth and high energy taxes will boost government revenues in 2023. Current spending is expected to grow less than nominal GDP, due to government wage moderation. Public investment as a percentage of GDP is expected to increase due to ambitious domestic fiscal targets and a large inflow of EU funds. Additional payments to pensioners, changes in the tax code, the compensation scheme to cope with rising energy prices and credibly announced legislation to reduce government spending by 2023 are all included in the forecast.

The deficit is expected to narrow to about 4.4 percent of GDP in 2024, as current spending as a percentage of GDP declines due to the discontinuation of some measures implemented in 2022/2023 that amount to about 0.3 percentage points. Nominal economic growth is expected to remain substantial. Growth in capital spending is expected to slow down due to the base effect caused by the large residual of the 2014-2020 EU budget cycle expected in 2023. The Commission currently assumes a complete phase-out of energy support measures by 2024.

Public debt is expected to fall to 45.6% of GDP in 2023 as a result of deficit reduction before rising to 46.1% in 2024. Risks to the fiscal outlook are downside. Lower GDP growth, the upcoming election cycle, possible upward pressure on government wages due to negative real growth rates in 2021, pension indexation that will deal with the high inflation of 2022 in 2024 may lead to budget deficits.